By Václav Lorenc · CEO, Byzkids · Published June 16, 2026

AI as the New Interface Layer inspired by Banking

A Byzzard Blueprint mapping four AI maturity levels — from basic chatbot support to fully conversation-first banking — with real-world innovations, KPIs, an implementation roadmap, and an action checklist for banking and lending leaders.

1. Executive Summary

❗Important❗

The interface is shifting. Users no longer navigate menus to find what they need — they state intent, and AI assembles the answer, action, or workflow. Banks that treat this only as a chatbot upgrade are misreading the shift. The real move is from navigation-first to intent-first.

Traditional mobile banking apps are built around screen hierarchies: the user learns the product structure and navigates to what they need. The AI interface layer model inverts this. Users express intent — in text, voice, or implicit behaviour — and AI interprets context, data, and next-best action to assemble the right response.

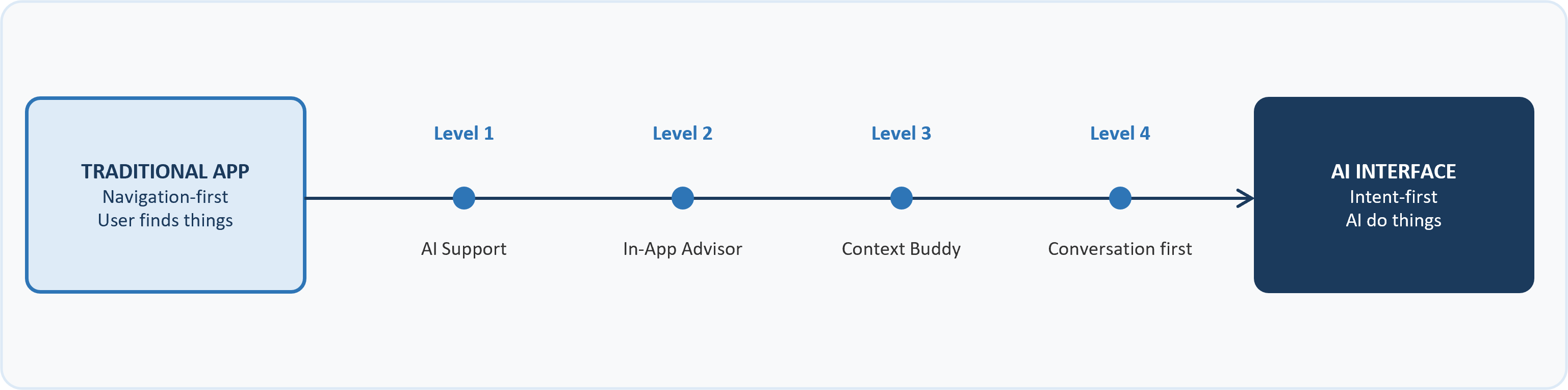

This blueprint maps four distinct maturity levels, from basic automated support to fully conversation-first apps, using real-world examples from banking and lending. It is designed to help banking leaders locate where they are today and identify the highest-value next move.

Key Takeaways

- Most banking apps today treat AI as an add-on chatbot that answers FAQs. The real shift is structural: AI becoming the primary interface through which customers discover, transact, and get help — replacing menus and screen navigation with intent and conversation.

- The highest short-term return for most banks is making the AI assistant data-aware: connecting it to live transaction and account data so it can complete real tasks inside the conversation, without redirecting users to other screens. This single move separates reactive chatbots from genuinely useful assistants.

- Lending is the biggest untapped opportunity in this space. Credit top-ups, pre-approvals, and limit increases are high-value, high-emotion moments that remain stuck in clunky multi-screen flows at most banks — and are well-suited for end-to-end conversational completion.

- The disintermediation risk is real and accelerating: OpenAI now lets users complete purchases directly inside a ChatGPT conversation, with the bank invisible beneath. AI-native companies are building the layer above financial services — the customer intent layer — and banks risk being reduced to a payment utility underneath.

- The strategic question every banking leader should be asking is not "should we add a chatbot" but "who will own our customers' financial intent in three years — us, or an AI-native company that got there first?"

2. The Shift: From Navigation to Intent

❗Important❗

Traditional apps make users find things. AI interface apps find things for users. The shift is structural — from menus and screens as the primary interaction model, to intent, context, and conversation. The four modes below map directly to the four maturity levels in this blueprint.

Traditional app interfaces assume the user knows where to go. They are built around menus, tabs, and screen hierarchies. The user's job is to navigate; the system's job is to wait. The cost of this model is hidden: every user who fails to discover a feature, abandons a journey, or calls a contact centre is a navigation failure, not a product failure.

AI as an interface layer changes this contract. The user states intent — naturally, imprecisely, sometimes incompletely — and the system interprets context, retrieves relevant data, and assembles the right action or answer. The screens become a result surface rather than a navigation system.

The structural shift

Four Interface Modes — Aligned to the Four Maturity Levels

Level 1: AI Support — A copilot sitting on top of the existing app. The underlying screens are unchanged; AI handles FAQs, routes queries, and automates first-line responses. The user still navigates — AI just reduces the steps before they find what they need. Low risk to ship, low transformation delivered.

Level 2: In-App Advisor — The UI itself reshapes based on AI inference. The home screen shows different content on payday vs. mid-month, or when a large expense is upcoming. Navigation persists but is pre-answered before the user navigates. The assistant links to live customer data and can complete end-to-end processes inside the chat thread.

Level 3: Context Buddy — A single input collapses navigation. The user types or says "Send €200 to Tom" or "Show my last three months of subscriptions" and the app resolves it. A full LLM model is connected to customer context. Screens become a result state. The assistant is the primary — not auxiliary — channel within the app.

Level 4: Conversation first — No trigger needed. The system monitors context — a suspicious transaction, an upcoming bill, a credit score change — and proactively intervenes. Voice and text replace navigation entirely. The app becomes a custom omnichannel agent with memory across sessions and channels. The most powerful and privacy-sensitive mode.

3. The Four Maturity Levels

Level 1 — AI Support

❗Important❗

Level 1 is table stakes. Most banks already have some version of it. The real question is not whether you have a chatbot — it is whether your assistant knows anything meaningful about the user it is talking to. Quality of escalation logic and personalization depth are the only differentiators at this level.

What defines this level

- Reactive only — user must initiate every interaction; the assistant never reaches out first

- Rules-based or basic NLP logic; no access to live customer account or transaction data

- FAQ and menu-tree navigation; handoff to human support agent at a fixed complexity threshold

- AI is bolted onto the existing interface as an additional channel, not integrated into it

- Outputs are text-only; no actionable elements, visualisations, or in-chat transactions

What it looks like in banking & lending

A chat bubble in the corner of the banking app that answers questions about branch hours, card blocking, overdraft limits, and basic payment queries. The assistant has no knowledge of the specific user's balance, recent transactions, credit status, or active products. Every answer is generic. The user still navigates to complete any real task. In lending, it answers "what is a personal loan" but cannot tell the user whether they qualify, what rate they would receive, or how to apply.

Innovation Example

AI-Powered Virtual Assistant | Verizon · USA

Verizon deploys an AI-powered in-app assistant that goes beyond reactive FAQ handling by predicting what customers are likely to ask before they type it. The assistant analyses the context of the user's current session — which screen they are on, what account events have occurred recently, and what actions similar customers typically take in the same context — to proactively surface the most probable next query as a suggested prompt. This predictive intent layer means the assistant does not wait for the user to formulate and type a question; it narrows the likely interaction space and reduces the effort required to get help. Practical use cases include managing plan upgrades, adding new lines, resolving billing queries, and navigating to the relevant part of the app for a specific task. While the assistant operates primarily on a reactive basis and does not yet complete E2E transactions autonomously, the predictive framing demonstrates how Level 1 AI can materially improve perceived intelligence and response speed without requiring full data integration.

AI assistant with predictive question suggestions

by Verizon

Verizon USA embeds an AI assistant that predicts likely questions from live app context, recent account events, and peer behavior. It suggests the next best prompt before users type, making support feel faster, smarter, and easier to navigate.

Key gap: Most banks already have some form of Level 1. The differentiation is in escalation logic quality and the ability to recognise when to move proactive — the bridge to Level 2. The step from Level 1 to 2 requires connecting the assistant to live account data; without that, no amount of NLP improvement changes the fundamental limitation.

Level 2 — In-App Advisor

❗Important❗

Level 2 is where the highest short-term ROI sits for most incumbents. The assistant gains access to real customer data and begins to act — not just respond. The key differentiator is E2E process completion inside chat, with no redirect to other screens. Lending journeys remain the least-explored E2E opportunity at this level.

What defines this level

- Linked to live customer transaction data, account balances, and product holdings

- Proactive outreach — AI initiates contact when a relevant event or trigger occurs in customer data

- E2E process completion within the chat thread — no redirect to other app screens required

- Visualised outputs alongside text: charts, payment breakdowns, actionable buttons, confirmations

- Built on top of the existing app structure; the app shell and navigation remain available

- Agentic capability begins: the assistant can initiate system actions, not just retrieve information

What it looks like in banking & lending

The assistant notices a large upcoming direct debit three days before it is due, proactively flags it, and offers to move funds from savings or set a payment reminder — entirely inside the chat thread. In lending: the user types "I want to increase my credit limit" and the entire journey — eligibility check based on live account data, offer presentation with rate and limit options, digital contract, and confirmation — completes without leaving the chat. No screen redirects. No separate application form. This is the highest-value untapped E2E flow for most banking apps today.

Innovation Examples

Erica — Proactive In-App Advisor | Bank of America · USA

Bank of America's Erica represents the most complete Level 2 deployment in retail banking. The assistant accesses live transaction data and account history to power proactive financial move recommendations — including alerts when the user is close to a spending threshold, when a bill increases unexpectedly, or when a savings opportunity is identified based on spending patterns. Users can complete full banking transactions — transfers, payments, card management, dispute initiation — entirely inside the chat interface with no redirect to other screens. Responses include visualised outputs such as spend charts, payment schedules, and balance breakdowns alongside text. Actionable elements — confirm, schedule, reject — are embedded directly in the conversation. Proactive scenarios include credit score monitoring, subscription management nudges, and personalised savings suggestions.

Behavior-based tips

by BofA

Bank of America USA upgraded its digital assistant, Erica, to deliver smarter spending tips, track subscriptions, monitor credit, and guide users through behaviorbased interactions.

AI Agent Payments in Wallet | PayPal · USA

PayPal integrates Mastercard Agent Pay into its wallet, enabling AI agents to execute financial transactions on behalf of users autonomously. When a user interacts with an AI assistant — inside or outside the PayPal app — the agent can initiate, authenticate, and complete a payment without the user navigating to a checkout screen. The architecture separates intent (expressed conversationally) from execution (handled by the agent), with PayPal acting as the trusted transaction layer. This is the clearest production signal that agentic action — not just conversational response — is the next frontier for Level 2, and that banks who do not build agent-compatible payment infrastructure risk being bypassed entirely.

AI Agent payments in wallet

by PayPal

PayPal USA integrates Mastercard agent pay into its wallet, enabling AI agents to perform transactions for users, providing a seamless and secure checkout experience.

AI-Driven Item Suggest via Photo/Barcode | Klarna · SWE

Klarna introduces an AI-driven feature that allows users to photograph a product or scan its barcode directly within the app. The AI then searches across Klarna's merchant network and returns a list of visually and functionally similar items available at lower prices, sorted by discount and merchant rating. The feature does not simply improve an existing screen — it creates an entirely new interaction category that would not exist without AI: shop-by-image. This represents a structural expansion of the interface rather than an incremental improvement, demonstrating how Level 2 AI can unlock feature categories that are impossible in a traditional navigation-first app model.

Photo-to-shop AI search

by Klarna

KlarnaSWE introduced an AIdriven feature in its app that enables users to photograph a product or scan its barcode. The app then suggests similar items at a more affordable price.

Key gap: Proactive trigger design is the critical risk at Level 2. Getting it wrong — outreach that is too frequent, poorly timed, or irrelevant — creates distrust faster than any technical error. The discipline of defining exactly which events justify an unsolicited notification, and what action the user is expected to take, is where most implementations fail. Lending-specific E2E flows — credit top-up, pre-approval, limit increase — remain almost entirely unmapped by incumbents.

Level 3 — Context Buddy

❗Important❗

Level 3 is where challenger banks are today and incumbents will be in two to three years. The assistant moves from scripted flows to open-ended LLM understanding, with full customer context injected. Hallucination risk in a regulated financial environment is the non-negotiable engineering challenge. The LLM partnership model — not in-house model building — is the realistic path for most banks.

What defines this level

- Full LLM model access — open-ended natural language understanding beyond scripted or ruled flows

- Customer context injected into the model at request time: balance, transaction history, risk profile, life stage signals

- The assistant is the primary — not auxiliary — communication channel within the app structure

- Peer benchmarking and personalised insights: user's data compared against anonymised cohort benchmarks

- Multimodal input: image upload, document processing, voice, and barcode scanning

- AI surfaces relevant app features contextually in response, replacing the need for the user to navigate

What it looks like in banking & lending

The user asks "Am I spending more on food than people like me?" and receives a peer-benchmarked spending comparison with a personalised savings suggestion. Or: the user photographs their payslip, asks "Can I afford a bigger mortgage?" and the LLM processes the document, cross-references the existing account data and outstanding commitments, and returns a grounded eligibility assessment — not a generic calculator. In lending: the assistant proactively surfaces a pre-approved credit top-up at a moment of detected financial stress — a large transaction combined with a low balance — and walks the user through confirmation in two conversational turns.

Innovation Examples

Finn — LLM-Linked Context Buddy | Bunq · NLD

Bunq's Finn is connected to an external LLM and injected with the user's full account context at query time. This enables Finn to answer questions that extend well beyond traditional banking — travel recommendations, tax implications of a transaction, weather at a destination, budget planning for a life event — while grounding every financial response in the user's actual data. Finn can compare spending against anonymised peer cohorts and deliver genuinely personalised recommendations rather than generic tips. Users can upload images and documents and Finn can process them as a standard LLM would. In many responses, Finn identifies relevant features already available in the Bunq app and surfaces them contextually, replacing the need for navigation. One of the most complete Level 3 deployments among European challenger banks.

AI coach with full account context

by Bunq

Bunq NLD equips Finn with full account context and an external LLM to answer banking, travel, tax, and life-planning questions in one chat. It even reads images and surfaces app features, turning support into a deeply personal financial coach.

AI-First Digital Banking Assistant | Ryt Bank · MYS

Ryt Bank introduces an AI-powered digital banking assistant that enables users to conduct full banking transactions — transfers, payments, account queries, product applications — entirely through natural language conversation, without navigating any traditional screen flows. The assistant operates in multiple languages with cultural and linguistic nuance, enabling accessibility across a multilingual user base that a screen-navigation model would struggle to serve. The architecture makes the AI assistant the primary interface of the entire banking product rather than a supplementary channel. Ryt Bank demonstrates that conversation-first banking is already live and in production in emerging market challengers, where the gap between traditional navigation UX and conversational AI is largest.

Digital banking as an AI assistant

by Ryt Bank

Ryt Bank MYS introduces an AI powered digital banking assistant enabling users to conduct transactions through natural conversation in multiple languages, enhancing accessibility with advanced linguistic capabilities and cultural understanding.

Chatbot-First Financial App | Cleo · GBR

Cleo builds its entire app proposition around a chatbot interface rather than a traditional screen hierarchy. Every customer interaction — spending summaries, budget setting, savings goals, financial advice, roasting or cheerleading spending behaviour — happens through a conversational thread. Alongside the bot, Cleo retains a minimal tab structure for users who prefer structured data access, but the chat is the primary experience and the one Cleo actively designs for. To reduce the blank-input problem — users not knowing what to ask — Cleo surfaces tips and prompts in the chat feed in a social media story format: short, themed cards that act as conversation starters rather than static content. A user tapping "All about your budget" or "Hype me" enters a guided conversational flow tailored to their actual transaction data. This design pattern directly addresses the discoverability challenge of chat-first interfaces: instead of waiting for users to think of a query, the interface serves contextual prompts that make the first interaction obvious.

Chat-first interface for comprehensive financial management

by Cleo

Cleo GBR makes chat the main interface for budgeting, savings, advice, and even playful money coaching, with tabs only as backup. Story-style prompt cards spark guided conversations from real transaction data, making finance feel intuitive and habit-forming.

Story-Based Investing | Zeed AI · USA

Zeed AI reimagines retail investing as an interactive video and conversation experience. Users watch short AI-generated video insights on individual stocks, sectors, and themes — built from real market data and personalised to portfolio holdings. Within each video, users can ask questions directly in natural language, dig deeper into a specific data point, or execute a trade without leaving the experience. The interface connects portfolio data, market intelligence, and a conversational AI layer into a single content-first flow. This represents a different expression of the Level 3 model: rather than replacing navigation with chat, it replaces navigation with content — AI-created video becomes the access layer to both information and action.

Storybased investing

by Zeed AI

Zeed AI USA turns finance into interactive video, letting retail investors watch insights, connect portfolios, ask questions, and trade directly in a storylike format built for education and action.

Perplexity AI Search Built into Mobile App | Deutsche Telekom · DEU

Deutsche Telekom integrates Perplexity AI's search and answer engine directly into its mobile app, giving Telekom subscribers free access to Perplexity's AI models as a built-in feature of their mobile plan. Customers open the Telekom app and can immediately query Perplexity's LLM — which combines real-time web retrieval with generative responses — without a separate subscription, login, or app. The integration positions AI search not as a premium add-on but as a core service benefit tied to the mobile relationship. For Telekom, this creates a tangible differentiation argument at point of acquisition and renewal: the network now bundles intelligence, not just connectivity. The model is directly applicable to banking: a bank that integrates a leading LLM as a free benefit of holding an account — available from inside the banking app, grounded in account context — converts a commodity financial relationship into an AI-powered daily utility. This is the partnership shortcut to Level 3 for institutions that cannot build proprietary models in a realistic timeframe.

Inapp smart search

by Deutsche Telekom

Deutsche Telekom GER offers customers free AI search in the MeinMagenta app, providing realtime answers, curated articles, and Pro perks, enhancing the customer experience with advanced AI tools.

Key gap: Hallucination risk in a financial context carries regulatory and trust consequences that do not exist in general-purpose AI applications. A banking LLM that confidently returns an incorrect balance, a wrong rate, or a misinterpreted product condition creates compliance exposure, not just a UX failure. Retrieval-augmented generation (RAG) grounding against live account data and product documentation, combined with strict output guardrails and human-review escalation paths, are non-negotiable engineering requirements at this level.

Level 4 — Conversation First

❗Important❗

Level 4 is where the bank stops being a product with an AI feature and becomes an agent with a banking licence. The OpenAI shopping checkout is the clearest external signal: if AI-native companies own the customer's intent layer, banks become the payment rail underneath, not the relationship above. The window to position as the trusted agent is open but closing.

What defines this level

- Text and voice are the primary input modalities; screens are a result surface, not a navigation system

- AI assembles the entire journey on demand — no fixed screen flows or predefined navigation trees

- Smart keyboard suggestions in-chat and swipe-accessible panels for core data (card details, transactions)

- Cross-channel continuity: app, web, IVR, and branch interactions share the same agent context and memory

- Proactive ambient monitoring: the system initiates without any user trigger, based on event detection

- The underlying backend and APIs are unchanged; AI is the orchestration layer sitting above them

What it looks like in banking & lending

The home screen is a chat input with a welcome message and real-time account summary. The user types or speaks any intent and the app resolves it completely. Static screens exist only as swipe-accessible panels for high-frequency reference data — card numbers, recent transactions. In lending, a user says "I need €3,000 for home repairs" and the agent checks eligibility against live data, presents two or three product options with rates and monthly payments, takes the user's selection, completes KYC validation, presents a digital contract, receives confirmation, and disburses funds — all within a single conversation thread, in under five minutes.

Innovation Examples

Conversation-First Banking App | Liveperson · USA

Liveperson's banking interface replaces the traditional home screen with a chat input and a contextual welcome message that includes a live account balance summary. All user inputs are entered via text or voice; a smart suggestions keyboard surfaces next-word and next-intent completions as the user types. The AI resolves every query — transfers, balance checks, bill payments, product enquiries, travel notifications — within the chat thread. Responses are either conversational text or prepared visual outputs that mirror the layouts of standard app screens but appear inline in the conversation. Users can swipe left or right to access predefined panels for card details and transaction history, preserving the ability to access structured data without navigation. Every AI response includes contextually suggested follow-up actions, creating a guided conversational flow rather than a dead-end answer. Past conversations are stored and searchable, giving the chat history a dual function as both a service record and a personal financial log.

Chat-first banking with balance-aware conversational interface

by LivePerson

LivePerson USA turns banking into a chat-first experience with balance-aware greetings, smart text and voice input, and inline screen-like answers. Searchable history and guided next steps make every interaction feel continuous, fast, and highly intuitive.

ChatGPT Shopping Checkout | OpenAI · USA

OpenAI launches an integrated shopping and payment function within ChatGPT, allowing users to complete purchases directly inside a chat conversation. Initial availability covers US Etsy shoppers with committed expansion to Shopify merchants. The user expresses purchase intent conversationally, the AI surfaces relevant products, and the transaction completes without the user leaving the ChatGPT interface. The payment infrastructure runs beneath the surface — the bank processes the transaction but is invisible to the user experience. This is the most important disintermediation signal in the dataset: an AI-native company is building a commerce interface in which the customer relationship, product discovery, and checkout all occur within the AI layer, and the bank is reduced to a payment utility. Banks that do not establish themselves as the trusted agent layer before this pattern becomes mainstream will find themselves structurally below the customer relationship, not above it.

Shopping checkout built into chat

by OpenAI

OpenAI USA launches an online shopping payment function for ChatGPT, allowing users to complete purchases directly in chat with initial availability for US Etsy shoppers and future support for Shopify merchants.

Key gap: Legacy UX migration is the hardest operational challenge at Level 4. Existing customers are trained on screen navigation; a hard switch creates confusion and measurable churn. The winning pattern observed in early deployments is gradual interface transition — conversation-first as the default for new users and for new product categories, with screen-based navigation retained as a fallback for existing users — rather than a forced replacement. The regulatory challenge is equally significant: a conversation-first interface that surfaces product recommendations at scale enters advisory territory that triggers MiFID II, PSD3, and local CNB/NBS obligations.

4. Cross-Cutting Themes

❗Important❗

Three themes cut across all four levels and should inform every investment decision in this space: the structural distinction between an AI interface and an AI feature; the lending E2E opportunity that remains almost entirely unmapped; and the disintermediation risk that makes waiting a losing strategic position.

AI interface vs. AI feature

The most common misread: a bank adds a chatbot, calls it an AI interface, and benchmarks itself against Level 3 competitors. The distinction is structural. A feature is additive — it sits alongside the existing product. An interface layer replaces part of how users interact with it. The test is simple: can the user complete their most common tasks without ever leaving the conversational layer? If the answer is no — if even a transfer or a balance check requires a screen redirect — it is a feature, not an interface.

Lending as the highest-value E2E opportunity

Credit top-up, pre-approval notification, limit increase, and repayment flexibility are high-emotion, high-value moments that customers currently navigate through clunky multi-screen flows. None of these journeys have been meaningfully redesigned for conversational completion by incumbents. A bank that can deliver a pre-approved credit top-up in two conversational turns, with a single confirmation tap, will have a structural engagement and conversion advantage that is very difficult for competitors to replicate quickly. The data infrastructure requirement — live account and credit data available to the assistant at query time — is also the main barrier, making early investment in data connectivity a prerequisite for the lending E2E opportunity.

The disintermediation risk

OpenAI's shopping checkout and PayPal's agentic payments point to the same structural outcome: AI-native companies are building the intent layer above payments and financial services, with banks as the silent infrastructure underneath. The window for banks to position themselves as the trusted agent layer — the entity that holds the customer's financial intent, memory, and relationship — is open now but closing. Waiting for conversation-first to become the mainstream expectation before investing is the losing position; by the time it is mainstream, the relationship will already belong to someone else.

Build vs. partner vs. white-label

For most incumbents, building a proprietary LLM is not commercially viable. The realistic options are: (1) partnership with a leading LLM provider with deep customer context integration — as Deutsche Telekom is doing with Perplexity, bundling AI search as a built-in app benefit rather than a feature add-on; (2) white-label conversational AI platforms with banking-specific guardrails and regulatory compliance baked in; or (3) embedding open-source models with bank-controlled retrieval layers (RAG) that ground responses in validated product and account data. The choice should be driven by data sensitivity requirements and time-to-market pressure, not by a preference for building over buying.

5. KPIs & Success Metrics

❗Important❗

Start with three high-leverage metrics: assistant task completion rate (target >60%), E2E in-chat completion rate for transactional flows (target >50%), and proactive action rate on triggered notifications (target >25%). These three metrics span adoption, capability, and proactive value — and together reveal which maturity level you are actually operating at, regardless of what your roadmap says.

Instrument these metrics from day one, separated by maturity level. Track leading indicators (predictive, act now) separately from lagging indicators (confirm strategy is working). The key insight: measure not just assistant usage but task completion and downstream financial behaviour.

Adoption & Engagement Metrics

| KPI | Type | What to Measure | Target / Benchmark |

|---|---|---|---|

| Assistant Session Rate | Leading | % of monthly active app users who open the assistant at least once |

30% MAU |

| Query Completion Rate | Leading | % of assistant sessions that reach a satisfactory resolution without human escalation |

60% |

| Escalation Rate | Leading | % of sessions handed off to human agent | Track; reduce quarter on quarter |

| Return Engagement | Lagging | Share of users who use the assistant again within 7 days of first session |

50% within 7 days |

Task Completion & Conversion Metrics

| KPI | Type | What to Measure | Target / Benchmark |

|---|---|---|---|

| E2E In-Chat Completion | Leading | % of transactional intents (transfer, top-up, limit increase) completed without leaving the chat thread |

50% of transactional sessions |

| Lending Journey Conversion | Lagging | % of credit top-up / limit increase intents expressed in chat that result in a completed transaction |

35% |

| Screen Redirect Rate | Leading | % of assistant responses that require the user to navigate to another screen to complete the task | Track; reduce to <20% |

| Feature Discovery via AI | Lagging | % of users who access a product feature for the first time through the assistant rather than through navigation | Track; grow quarter on quarter |

Proactive AI & Trust Metrics

| KPI | Type | What to Measure | Target / Benchmark |

|---|---|---|---|

| Proactive Action Rate | Leading | % of proactive AI notifications that result in the user taking the suggested action within 24 hours |

25% |

| Proactive Opt-out Rate | Lagging | % of users who disable proactive AI notifications after receiving them | <10%; spike signals poor trigger design |

| AI Output Trust Rate | Lagging | Post-interaction survey: "Did the AI give you accurate information?" |

85% yes |

| Assistant NPS | Lagging | Net Promoter Score measured specifically for the AI assistant experience, separate from overall app NPS |

40 |

6. Implementation Roadmap

❗Important❗

Quick wins ship in weeks: connect the assistant to live account data and map one E2E lending journey for in-chat completion. These two moves deliver the largest step-up in perceived AI quality with the least architectural change. Deeper LLM integration and conversation-first redesign follow in later phases once internal data pipelines and trust guardrails are in place.

Structured in four phases from quick wins to strategic transformation. Each phase builds on the previous and delivers independent value — the roadmap does not require completing a phase before the next delivers results.

| Phase | Timeline | Key Deliverables |

|---|---|---|

| Quick Wins | Weeks 1–8 |

|

| Foundation | 1–3 months |

|

| Context & Personalisation | 3–6 months |

|

| Conversation First | 6–18 months |

|

7. Action Checklist

❗Important❗

Your single highest-impact first action: connect your existing assistant to live transaction data. Without that connection, no amount of NLP improvement or UX polish changes the fundamental quality of every interaction. Start there, then instrument everything so you know which move to make next.

Translate this blueprint into concrete next steps. Use this as a starting agenda for your next product planning session.

Diagnostic — Understand Where You Are

- Audit your current assistant: can users complete a transfer, check a balance, and report a lost card without leaving the chat thread? If not, you are at Level 1.

- Map which customer data the assistant can access today: if it cannot see live account data, transaction history, or product holdings, data connectivity is the first priority.

- Instrument your assistant usage now: query categories, escalation rate, completion rate, and session length are the four minimum metrics needed to baseline and improve.

- Identify the three highest-volume assistant queries today — these are the first candidates for E2E in-chat completion.

Level 1 → 2 — Connect and Complete

- Connect the assistant to live account data: balance, transactions, product holdings, credit status. Read-only access is sufficient to start.

- Map one full lending journey — credit top-up, limit increase, or pre-approval — step by step. Identify every screen redirect and plan to eliminate them.

- Define one proactive trigger with a specific event condition, message template, and attached action. Test with a 5% pilot segment before scaling.

- Add visualised outputs to the assistant: at minimum, balance charts, spend breakdowns, and payment confirmations should appear inline in the chat thread.

Level 2 → 3 — Bring in the LLM

- Evaluate LLM partnership options: identify two or three external providers and assess data privacy, regulatory compliance, and customer context injection capability.

- Define the RAG grounding architecture: which product documents, rate sheets, and policy texts need to be available to the LLM at query time to prevent hallucination.

- Build output guardrails before deploying any LLM to customers: define what types of statements require human review or factual verification before display.

- Pilot peer benchmarking for one spend category: food, transport, or subscriptions. Measure engagement lift vs. generic tips.

Level 3 → 4 — Go Conversation-First

- Design a conversation-first onboarding path for new users: test a chat-home experience with a pilot cohort before rolling out to the full base.

- Map the ambient AI trigger taxonomy: which financial events justify proactive contact without a user-initiated session?

- Assess regulatory obligations for recommendation-grade outputs: identify where CNB/NBS advisory rules apply to AI-generated responses and plan the compliance layer.

- Explore the Byzzard platform for additional Level 3–4 innovations: 40+ examples with implementation detail available at byzzard.com.

Ready to go deeper?

Explore the full interactive innovation flows on the Byzzard platform, benchmark your app's AI maturity against market leaders, and access detailed implementation cards for every example referenced in this blueprint.

Frequently asked questions

Related blueprints

Book a demo for free

Want to experience whole Byzzard innovation hub?

Get access to 2,000+ innovations, blueprints on various topics and our closed AI model APEX for free.