By Václav Lorenc · CEO, Byzkids · Published May 5, 2026

Mobile Account Opening in Banking Apps

A Byzzard Blueprint for digital banking leaders seeking to optimize their mobile onboarding experience, reduce drop-off rates, and benchmark against market innovators.

BLUEPRINT AT A GLANCE

- Topic: End-to-end mobile account opening for retail banking

- Audience: Product managers, digital banking heads, UX strategists

- Time to read: 10 minutes

- Innovations referenced: 6 real-world examples in playbook, 20+ in Byzzard database

1. EXECUTIVE SUMMARY

❗Important❗

A best-practice mobile account opening experience is a fast (<5 min) end-to-end flow that minimizes taps using BankID/eID or OCR/liveness, prioritizes same-day activation (first deposit or payment).

A best-practice mobile account opening experience is a fast (<5 min), the process starts with the first app open and ends with the first real customer experience – the first payment. Whole process minimizes number of taps to finish by using BankID/eID + OCR/liveness instead of traditional photo capturing of IDs.

KEY TAKEAWAYS

- Target full mobile completion in <5 minutes with minimal taps — each removed field materially lowers abandonment

- BankID/eID-first verification removes keystrokes, reduces errors, and significantly increases completion

- Progressive verification: move non-critical KYC questions after activation where regulations permit

- Define one measurable “aha moment” (e.g., same-day virtual card payment) and make it trivially easy after approval

- Instrument every funnel stage — promo → first app open → verification → sign → first payment — to identify the single largest drop-off

- Passwordless + biometric auth from day one; step-up MFA only for high-risk actions

🔍 BYZZARD INNOVATION SPOTLIGHT — THE 80% REFERENCE

Why “80% reference”? If you replicate this single onboarding process bellow end-to-end, you will cover approximately 80% of the best-practice acquisition flow described in this playbook.

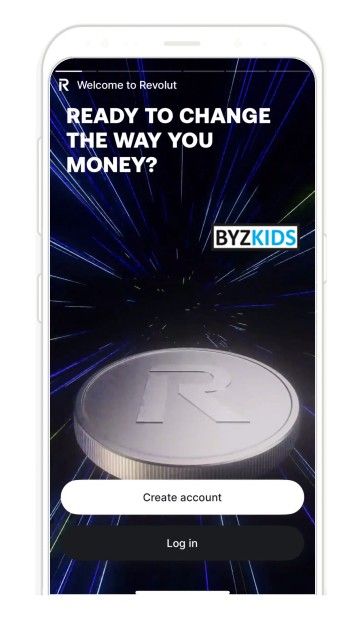

Near-Frictionless Onboarding with OCR Auto-Fill | Revolut · LTU

Revolut makes onboarding feel effortless by combining minimal form design with OCR auto-fill. Customers scan an ID, key details are filled automatically, and the flow removes the biggest cause of abandonment: manual input.

What to copy:

- Minimal field count

- OCR ID scan with instant auto-fill

- Camera-first onboarding

- Faster completion with less typing

- Lower drop-off through lower effort

Simlified onobarding in app

by Revolut

Revolut LTU delivers smooth onboarding by collecting only essential data and using fast OCR to scan IDs in seconds. Customers avoid long forms as details auto-fill instantly. The wow factor is near-frictionless signup, cutting drop-offs and making account opening feel effortless and modern.

2. TOPIC OVERVIEW & SCOPE

This blueprint covers the full mobile account opening journey for personal retail banking products — from promotional touchpoint through to a fully activated account with a completed first transaction. The scope includes current accounts, savings accounts, and basic deposit products opened entirely within a mobile banking application.

In scope

- Mobile-first account opening flows

- BankID/eID and OCR/liveness verification

- Document capture and identity assurance

- Onboarding UX, progress design, and activation

- Security: passwordless auth, device trust, adaptive MFA

- Existing and new-to-bank customers

- Same-day activation and first transaction mechanics

Out of scope

- Business / corporate account opening

- Branch-assisted or web-only flows

- Credit products (loans, credit cards)

- Country-specific regulatory deep-dives

- Investment or brokerage accounts

3. STRATEGIC CONTEXT

❗Important❗

Four forces are converging: embedded finance raising the competitive bar, digital identity frameworks enabling frictionless KYC, AI-first interfaces eliminating manual form entry, and invisible security replacing password friction. Banks that don’t adapt will lose digitally native customers to challengers delivering sub-3-minute activation.

Mobile account opening is rapidly shifting from a back-office digitization exercise to a front-line competitive battleground. The banks winning new customers today are those that treat onboarding not as a compliance process with a digital wrapper, but as their single highest-leverage conversion moment — the first impression that determines whether a prospect becomes an active, revenue-generating customer or abandons to a competitor. With challenger banks routinely delivering sub-3-minute account activation and fintechs embedding account-like products directly into non-banking platforms, the window for traditional banks to modernize their onboarding is closing. The strategic question is no longer whether to invest in mobile account opening, but how fast you can close the gap between your current experience and the new market standard.

Four industry mega-trends are converging to reshape what best-in-class account opening looks like:

1. Embedded Finance & Open Banking

PSD2/PSD3 and embedded finance are creating new competitive entry points where fintechs and non-banks offer account-like products with near-zero friction. Traditional banks that maintain lengthy, branch-dependent onboarding risk losing digitally native customers to challengers that promise instant activation. Implication: The competitive benchmark is no longer other banks — it is the last great digital signup experience customers had, whether a streaming service or a ride-hailing app.

2. Digital Identity & Regulatory Enablement

eID and national eID/BankID schemes are simultaneously tightening verification standards and enabling frictionless digital identity. Banks that adopt BankID/eID-first strategies gain both regulatory compliance and dramatically reduced onboarding friction — replacing manual data entry with one-tap verification that returns prefilled, verified data. Implication: Regulation is becoming an enabler, not just a constraint. Early adopters of digital ID frameworks turn compliance into a competitive UX advantage.

3. AI-First Interfaces & Intelligent Onboarding

AI is transforming onboarding from static forms into conversational, adaptive flows. OCR auto-capture, liveness detection, and intelligent pre-filling are becoming baseline expectations. Conversational data collection and smart defaults reduce form fields by 30–50% while improving data accuracy. Implication: Manual form filling is becoming a legacy pattern. Banks that don’t adopt AI-assisted onboarding will feel increasingly dated compared to both fintech competitors and non-banking digital experiences.

4. Invisible Security & Passwordless Authentication

Security is shifting from upfront friction gates to continuous, risk-adaptive protection. Device-bound credentials, behavioral biometrics, and FIDO2/WebAuthn are replacing passwords and SMS OTPs. The goal is maximum assurance with zero perceived friction for legitimate users. Implication: Security and convenience are no longer trade-offs. Banks that still force password creation during onboarding are adding unnecessary friction that directly increases drop-off.

4. REAL-WORLD INNOVATIONS & INSPIRATION

❗Important❗

Three proven results from leading banks: 88% of users completing via BankID with 40% fewer support tickets, 78% achieving full verification within 48 hours with 65% same-day activation, and 85% one-tap conversion with 72% same-day first deposit for existing customers.

The following examples are drawn from the Byzzard innovation database. Each showcases a distinct approach to solving common account opening challenges. Explore the full interactive flows on the Byzzard platform.

Emoji-Driven AML Question Flow | Monzo · GBR

Replaces complex compliance questions with clear multiple-choice answers paired with intuitive emojis. Instead of typing free-text explanations, customers tap a relevant option and move on. By reframing a regulatory requirement as a simple, friendly interaction, the operator removes one of the most friction-heavy moments in the onboarding flow without compromising compliance integrity. Result: reduced AML step drop-off, higher completion rates and improved user trust toward the bank.

Friendly AML

by Monzo

Monzo GBR simplifies AML checks by turning complex compliance questions into clear multiple-choice options with relevant emojis. Customers tap intuitive answers instead of typing long explanations. The wow factor is compliance made friendly, reducing friction while improving completion rates and user trust.

Instant Wallet Provisioning at Onboarding Completion | N26 · GER

Prompts customers at the final step of onboarding to add their new card to Apple Pay or Google Wallet with a single tap — before the physical card has even been dispatched. By collapsing the gap between account opening and first real-world usage, the operator turns the congrats screen into an immediate activation moment rather than a dead end. Result: zero wait time to first payment, higher same-day activation rates and a strong first impression that the account is ready to use right now.

Instant Wallet Push

by N26

N26 GER prompts customers at the end of onboarding to instantly add their card to Apple Pay or Google Wallet. With one tap, users can start paying before the physical card arrives. The wow factor is zero wait time, turning account opening into immediate real-world usage and delight.

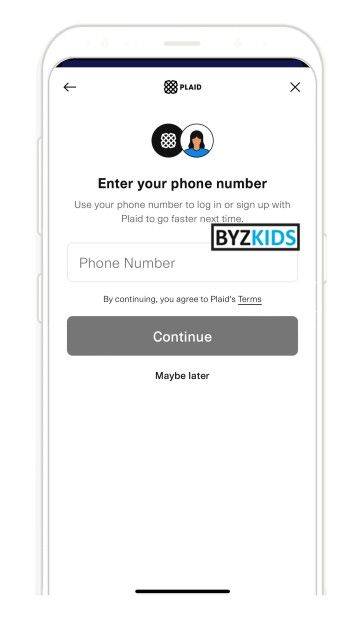

Cross-Bank Identity Verification | CLEO · GBR

Verifies customer identity by securely connecting to an existing bank account at another institution through Plaid, pulling real transaction data as proof of identity instead of relying on manual document uploads. The approach leverages a financial relationship the customer already has, making verification feel instant and effortless rather than bureaucratic. Result: faster identity confirmation, reduced manual review burden and higher onboarding trust for new users.

Cross-bank validation

by Cleo

Cleo GBR uses Plaid to verify customer identity by securely connecting to an existing bank account at another bank. It checks real transaction data instead of relying only on manual uploads. The wow factor is instant cross-bank validation, making onboarding faster and more trustworthy for users.

🔍 EXPLORE MORE ON BYZZARD

2,000+ additional innovations on banking mobile acquisition are available on the Byzzard platform, including full interactive flow walkthroughs and screenshot galleries.

5. KPIS & SUCCESS METRICS

❗Important❗

Start with three high-leverage metrics: completion rate (target >70%), time-to-account (<5 min), and same-day activation rate (>50%). These have the most direct impact on acquisition economics and are actionable within weeks.

Instrument these metrics across the full funnel — from promotional touchpoint through activation and retention. Separate leading indicators (predictive, act now) from lagging indicators (confirm strategy). The key insight: measure not just account creation but time to first meaningful action.

Funnel & Conversion Metrics

| KPI | Type | What to Measure | Target / Benchmark |

|---|---|---|---|

| Application Start Rate | Leading | % of promo/product page visitors who tap “Open Account” |

25% of visitors |

| Step Drop-off Rate | Leading | Conversion rate between each acquisition step | Identify and fix the single largest drop |

| Completion Rate | Leading | % of started applications reaching submission | 70%+ |

| Time to Account | Leading | Minutes from first tap to usable account | <5 min (full flow) |

| Time to Activation | Leading | Median time from install to first meaningful action (deposit/payment) | <24h, ideally same session |

Activation & Retention Metrics

| KPI | Type | What to Measure | Target / Benchmark |

|---|---|---|---|

| Same-Day Activation | Lagging | % of new accounts completing first meaningful action on day of opening |

50% |

| 7 / 30 / 90-Day Retention | Lagging | Retention of activated cohorts at key intervals | Track trend; activated vs non-activated |

| Cost per Acquired Account | Lagging | Total cost including marketing, support, manual review | Track trend downward |

| Onboarding NPS | Lagging | Post-onboarding satisfaction measured specifically for the opening experience |

40 |

Friction & Security Metrics

| KPI | Type | What to Measure | Target / Benchmark |

|---|---|---|---|

| Taps to Homepage | Leading | Number of taps from app open to account homepage | Minimize; benchmark competitors |

| Taps to First Payment | Leading | Number of taps from congrats screen to completed first transaction | Minimize; <5 taps ideal |

| ID Verification Success | Leading | First-attempt pass rate for BankID/OCR/liveness |

85% without manual review |

| Help Request Rate | Leading | In-flow support/chat triggers during onboarding | Track; reduce via UX fixes |

| Passwordless Login % | Lagging | % of logins using biometric/passwordless vs password |

80% |

6. CUSTOMER JOURNEY MAP

❗Important❗

The two biggest drop-off points are identity verification (camera failures, BankID errors, slow queues) and the post-approval step (no instant card, unclear next action). Fixing these two stages first delivers the largest conversion lift. Design rule: let users browse and start before requiring sensitive data.

The journey below maps the recommended mobile account opening flow from the customer’s perspective. Each stage highlights customer actions, common pain points, and specific innovation opportunities. The flow follows the best-practice sequence: Promo → First open → Lead capture → Verification → Details → Sign → Activation.

| STAGE | CUSTOMER ACTIONS | COMMON PAIN POINTS | INNOVATION OPPORTUNITIES |

|---|---|---|---|

| 1 Promo & First Open | Sees ad/referral, downloads app, opens for first time. Sees value proposition + “Open in X mins”. | Unclear value prop, no time estimate, generic landing. User doesn’t understand what they’ll get. | One-screen first open: clear value + time estimate + single CTA. Personalized offer based on acquisition channel. |

| 2 Lead Capture | Enters phone number or email. Receives verification code. | Too many fields upfront. No save-and-resume if interrupted. Duplicate data entry later. | Minimal capture (phone only). Local progress save for unstable networks. Smart resume on return. |

| 3 Identity Verification | Selects BankID/eID (one-click) or scans ID + selfie liveness check. | Poor camera guidance, multiple retakes, unclear errors, long processing. Overly strict KYC for low-risk products. | BankID/eID-first with one-click redirect returning prefilled data. OCR auto-capture + lightweight liveness. Clear fallback for failed automated checks. Microcopy explaining why ID is needed. |

| 4 Personal Details & AML | Reviews/confirms pre-filled data from BankID/OCR. Answers minimal AML questions. | Manual re-entry of data already scanned. Too many AML questions upfront. No edit capability on prefills. | 1-tap confirm of pre-filled data. Progressive verification: defer non-critical KYC to post-activation. Allow user edits on prefilled fields. |

| 5 Contract & Sign | Reviews product terms, accepts T&Cs, signs contract (one-button or hold-to-sign). | Information overload, legal jargon, multi-step acceptance. Signing feels heavy. | Plain-language T&Cs summary with key points highlighted. One-button or hold-to-sign. Inline help and live chat available. |

| 6 Activation & First Action | Sees congrats screen, sets PIN/biometrics, immediately prompted to “Add money” or “Make first payment.” | Logged out after completion. No instant card. Activation requires separate app reopens. Unclear next steps. | Keep user logged in. Instant virtual card + Apple/Google Pay provisioning. Instant top-up. CTA directly to first payment. Small first-use incentive. Create an interactive quest based onboarding |

UX DESIGN RULES FOR THE JOURNEY

- Show process length upfront: clear checklist/progress bar (“what’s left”) + micro-milestones to lower anxiety

- End with celebration: congrats screen that immediately nudges to first transaction, not a dead-end confirmation

- Save & resume + offline support: allow local progress save for unstable networks

- Explain sensitive steps: use microcopy to explain why ID/AML steps are needed and expected duration

- Provide in-flow help: inline help and live chat accessible without leaving the flow

🔍 BYZZARD INNOVATION SPOTLIGHT

Quest-Based Onboarding with Prize-Draw Incentive | Emma · GBR

Replaces passive onboarding tutorials with a series of interactive quests that guide new users through core app features during their first month. Each completed quest builds familiarity with a specific capability while creating a sense of progress. Users who finish all quests within 30 days of download enter a prize draw for a free annual premium account — shifting the incentive from upfront discounts to earned engagement. Result: new users explore the full product surface instead of settling into a single feature, driving deeper activation and higher upgrade potential.

.webp?v=1)

Engaging quests

by Emma

Emma GBR motivates new users to become familiar with the app by engaging them with quests. If completed within the first month after app download, clients are entered into a prize draw for an annual premium account.

7. SECURITY & AUTHENTICATION DESIGN

❗Important❗

Highest-impact security design: passwordless + biometrics as default from day one, device-bound credentials with hardware keystore, and risk-adaptive step-ups only when signals require it. Never force password creation during onboarding — it directly increases drop-off, focus on simpler PINs instead.

Security must be designed as a seamless part of the experience, not as friction gates. The goal: maximum assurance with minimum user effort. Move from upfront barriers to continuous, risk-adaptive protection.

SECURITY DESIGN PRINCIPLES

- Passwordless + biometrics as default: device-bound credentials for daily use; step-up MFA only for high-risk actions (large transfers, settings changes)

- Device trust & adaptive auth: implement hardware keystore (Secure Enclave / Android Keystore), device attestation (Play Integrity / App Attest), short-lived tokens

- Risk-adaptive step-ups: friction appears only when risk signals require it — based on device, IP, behavioral patterns. Tune false positive rates continuously

- Push over SMS: prefer signed push confirmations over SMS OTP. Let the app act as confirmation for web SSO / approvals

🔍 BYZZARD INNOVATION SPOTLIGHT

NFC Chip Reading | Lloyds Bank · GBR

Uses NFC chip reading from national ID cards and ePassports to complete KYC in under 60 seconds. The app guides the user to hold their document against the phone, reads biometric data directly from the chip, and cross-references with a live selfie. Implements device attestation (Play Integrity / App Attest) and hardware keystore for credential binding, ensuring verification runs only on trusted, unmodified devices. Result: 92% first-attempt success rate, under 3-minute total onboarding.

.webp?v=1)

Account opening via NFC

by Lloyds Bank

Lloyds Bank GBR allows new account opening in the app via passport scan using NFC technology. A new app feature enables autofill of key personal data, including name, title, date of birth, gender, and country of birth.

8. RISKS & MITIGATIONS

❗Important❗

Highest-impact risks: BankID/OCR vendor downtime blocks all new account openings until restored. Non-negotiable mitigations: multi-tier fallback (BankID → OCR → manual), lead capture at every fallback tier, and async processing for when the real-time verification API is down.

Anticipate these common failure modes and plan mitigations into your roadmap from day one:

| RISK | MITIGATION |

|---|---|

| Over-strict KYC → high drop-off | Move non-critical questions after activation; prefer BankID/eID to reduce manual entry. Progressive verification unlocks features over time. |

| Vendor failures (BankID/OCR) | Robust error logging, clear fallback manual flow, in-flow help. Capture lead/contact for remarketing if user abandons during vendor failure. |

| Security friction / false positives | Adaptive auth so friction only appears when risk is detected. Continuously track and tune false positive rates. A/B test BankID vs manual KYC paths. |

| No activation after opening | Keep user logged in post-opening. Immediate virtual card + wallet provisioning. CTA to first payment on congrats screen. Small first-use incentive if needed. |

9. IMPLEMENTATION ROADMAP

❗Important❗

Quick wins ship in weeks: value-prop screen, transparent flow with progress bar, BankID path optimization and basic funnel instrumentation. Foundation (OCR + liveness, session persistence, same-day activation) takes 1–3 months. Full maturity including adaptive auth, FIDO2 and behavioral biometrics is a 12-month journey.

Structured in four phases from quick wins to strategic differentiators. Each phase builds on the previous, delivering incremental value while moving toward the full best-practice flow.

| PHASE | KEY DELIVERABLES |

|---|---|

| Quick Wins Weeks | One-screen first open: value proposition + “Open in X mins” + single CTA BankID/eID path optimization: one-click selection + redirect flow Checklist/progress bar + congrats screen leading directly to first payment Instrument funnel drop-off and taps between each stage |

| Foundation 1-3 months | Device-bound credentials (Secure Enclave / Keystore) + token hygiene OCR + liveness vendor integration with clear fallback manual flow Offline save/resume with local progress persistence Same-day activation mechanics: virtual card + Apple/Google Pay + instant top-up Analytics: verification errors, same-day activation, retention cohorts |

| Risk & Scale 3-6 months | Risk engine / adaptive authentication based on device, IP, behavioral signals App attestation (Play Integrity / App Attest) integration SIEM integration for fraud monitoring and alerting Progressive verification: defer non-critical KYC post-activation |

| Strategic 6-12 months | FIDO2/WebAuthn rollout for phishing-resistant authentication Advanced behavioral biometrics for continuous authentication Continuous pentesting & bug bounty program Cross-channel SSO: app as authenticator for web sessions |

10. ACTION CHECKLIST

❗Important❗

Your single highest-impact first action: instrument step-by-step drop-off in your current funnel, identify the one stage losing the most applicants, and design a targeted fix for that stage. Everything else follows from there.

Translate this blueprint into concrete next steps. Use this as a starting agenda for your next product planning session:

- Audit your current funnel: instrument drop-off between promo → first open → verification → sign → first payment. Identify the single largest drop-off point.

- Measure time-to-activation: track median time from install to first meaningful action, not just account creation.

- Evaluate BankID/eID integration: if available in your market, make it the primary (default) verification path.

- Count your taps: measure taps to homepage and taps to first payment. Remove every unnecessary field and screen.

- Implement save-and-resume with offline support: ensure users can exit and return without losing progress.

- Design your activation moment: instant virtual card + wallet provisioning + “Add money” CTA immediately after congrats screen.

- Plan security architecture: device-bound credentials now; FIDO2/WebAuthn on the 6–12 month roadmap.

- Explore innovations on Byzzard: deep-dive into the referenced examples and discover additional approaches for your market.

Frequently asked questions

Related blueprints

Book a demo for free

Want to experience whole Byzzard innovation hub?

Get access to 2,000+ innovations, blueprints on various topics and our closed AI model APEX for free.